The Cash Flow Statement is a financial statement that provides information about the cash inflows and outflows of a company during a specific period. It helps assess a company’s ability to generate cash and its overall liquidity. The statement is divided into three main sections: operating activities, investing activities, and financing activities.

- Operating Activities: This section reports the cash flows resulting from the company’s core operations. It includes cash inflows from the sale of goods or services and cash outflows related to operating expenses, such as payments to suppliers, employee salaries, rent, and taxes. It also takes into account changes in working capital, such as accounts receivable, accounts payable, and inventory.

Positive cash flow from operating activities indicates that the company’s core operations are generating cash, while negative cash flow may indicate cash is being used to sustain day-to-day operations.

- Investing Activities: This section includes cash flows related to the company’s investments in long-term assets or investments in other companies. It includes cash inflows from the sale of assets like property, plant, and equipment, as well as cash outflows for the purchase of new assets or investments. It also includes cash flows from the acquisition or sale of subsidiary companies.

Positive cash flow from investing activities suggests that the company is generating cash by making profitable investments, while negative cash flow indicates cash is being used for capital expenditures or acquisitions.

- Financing Activities: This section focuses on cash flows related to the company’s financing activities. It includes cash inflows from sources such as issuing stocks or bonds, obtaining loans, or receiving cash from investors. Cash outflows may include dividend payments, stock buybacks, debt repayments, or returning capital to investors.

Positive cash flow from financing activities indicates that the company is raising capital, while negative cash flow suggests that the company is using cash to repay debt or distribute funds to investors.

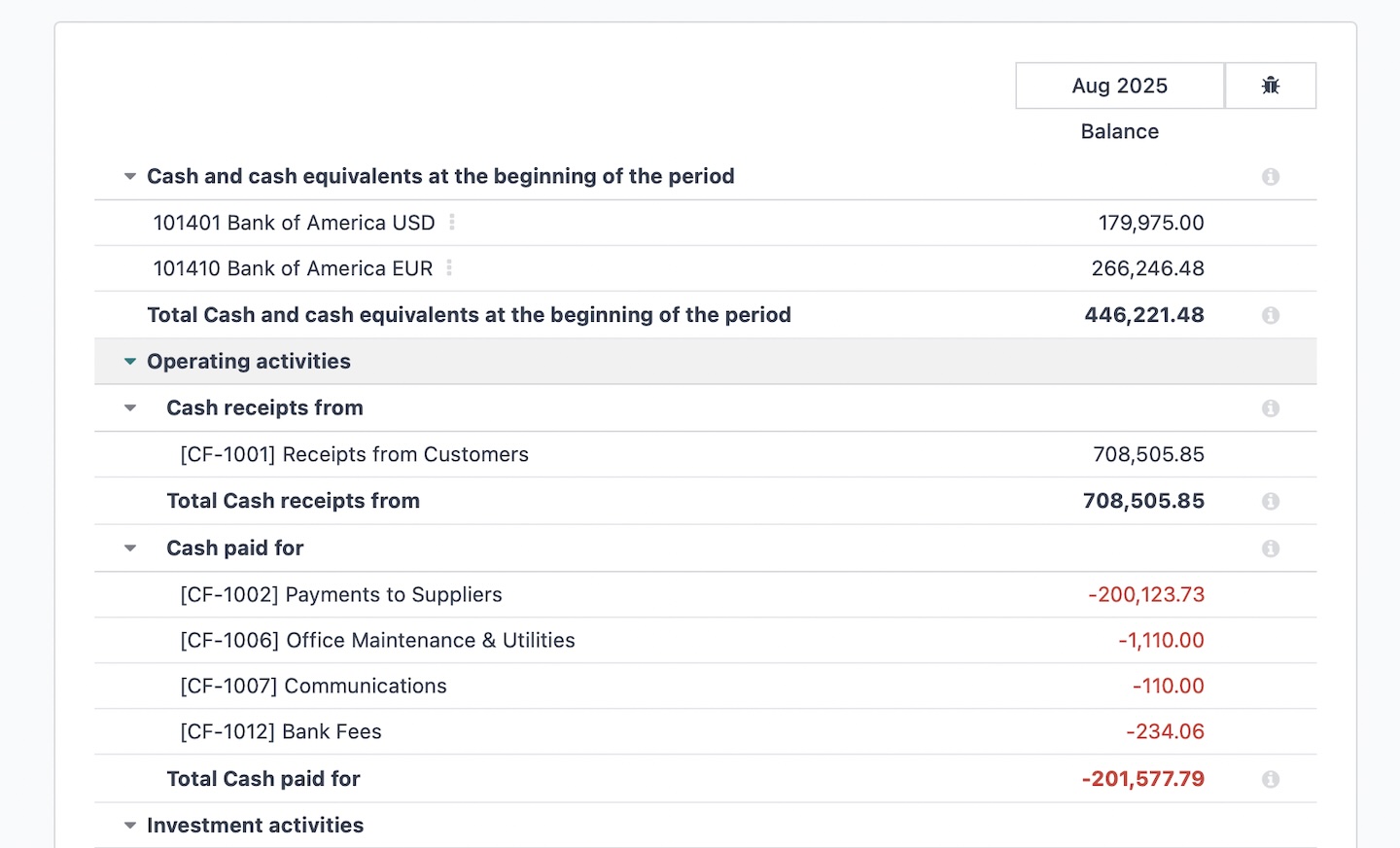

At the bottom of the Cash Flow Statement, the net increase or decrease in cash during the period is calculated by summing up the cash flows from operating, investing, and financing activities. This amount is added to the beginning cash balance to arrive at the ending cash balance.

The Cash Flow Statement helps investors, analysts, and creditors understand the sources and uses of cash by a company, providing insights into its financial health, cash generation capabilities, and ability to meet its financial obligations. It complements other financial statements such as the income statement and balance sheet, providing a comprehensive view of a company’s financial performance.

How the Cash Flow direct method works?

The direct method is one of the two approaches used to prepare the Cash Flow Statement, with the other being the indirect method. The direct method presents the actual cash inflows and outflows from operating activities, whereas the indirect method starts with net income and makes adjustments to convert it to cash flows from operating activities.

To understand how the direct cash flow method works, let’s focus on the operating activities section:

- Cash Inflows: Under the direct method, cash inflows from operating activities are reported by specific categories, such as:

- Cash received from customers: This includes cash collected from the sale of goods or services to customers.

- Cash received from interest and dividends: This includes any interest or dividend income received by the company.

- Cash Outflows: Similarly, cash outflows from operating activities are reported by specific categories, including:

- Cash paid to suppliers: This includes cash payments made to suppliers or vendors for the purchase of goods or services.

- Cash paid to employees: This includes cash payments made as salaries, wages, or other employee-related expenses.

- Cash paid for operating expenses: This includes cash payments for various operating expenses, such as rent, utilities, insurance, and taxes.

- Net Cash Flow from Operating Activities: The net cash flow from operating activities is calculated by subtracting the total cash outflows from the total cash inflows. This figure represents the net amount of cash generated or used by the company’s core operations during the given period.

It’s important to note that the direct method requires detailed information about cash receipts and payments, which may not always be readily available in a company’s accounting records. As a result, many companies opt for the indirect method, which starts with the net income figure and adjusts it for non-cash items and changes in working capital to derive the cash flow from operating activities.

Both the direct and indirect methods should ultimately produce the same net cash flow from operating activities, but the presentation and level of detail differ between the two approaches.

It’s worth mentioning that the direct method is encouraged by accounting standards (such as International Financial Reporting Standards or IFRS) as it provides clearer information about a company’s cash flows. However, the indirect method is more commonly used, possibly due to the challenges associated with gathering and presenting detailed cash flow information under the direct method.

The indirect method is an alternative approach to preparing the Cash Flow Statement. Unlike the direct method, which directly reports cash inflows and outflows from operating activities, the indirect method starts with the net income figure from the income statement and makes adjustments to convert it to cash flows from operating activities.

How the Cash Flow indirect method works?

Here’s how the indirect method works:

- Start with Net Income: The process begins with the net income figure, which is the bottom-line profit or loss reported on the income statement for the given period.

- Adjustments for Non-Cash Items: Certain non-cash items included in the net income need to be adjusted to reflect their cash impact. Common adjustments may include:

- Depreciation and amortization: These are non-cash expenses related to the wear and tear or the allocation of the cost of long-term assets over their useful lives. They are added back to net income since they do not involve actual cash outflows.

- Gain or loss on the sale of assets: Any gains or losses resulting from the sale of assets are removed from net income since they do not represent operating cash flows.

- Non-operating income and expenses: Income or expenses that are not related to the company’s core operations, such as interest income or interest expense, are adjusted to reflect their cash effects.

These adjustments help reconcile the accrual-based net income to the cash generated or used by operating activities.

- Changes in Working Capital: The next step involves analyzing changes in working capital accounts, such as accounts receivable, accounts payable, and inventory. The purpose is to determine how these changes impacted cash flows from operating activities. The general principle is that an increase in current assets (e.g., accounts receivable or inventory) will reduce cash flow, while an increase in current liabilities (e.g., accounts payable) will increase cash flow.

For example, if accounts receivable increased during the period, it implies that cash was tied up in unpaid invoices, resulting in a reduction in cash flow from operating activities. Conversely, if accounts payable increased, it suggests that the company delayed payments to suppliers, resulting in an increase in cash flow.

- Calculate Cash Flow from Operating Activities: By adding or subtracting the adjustments made for non-cash items and changes in working capital from the net income figure, the cash flow from operating activities is derived. This figure represents the cash generated or used by the company’s core operations during the given period.

- Cash Flows from Investing and Financing Activities: The indirect method also requires reporting cash flows from investing and financing activities separately, similar to the direct method. These sections involve reporting cash inflows and outflows related to investments in assets, acquisitions or sales of subsidiaries, issuance of stocks or bonds, repayment of debt, dividend payments, and other financing activities.

At the bottom of the Cash Flow Statement, the net increase or decrease in cash during the period is calculated by summing up the cash flows from operating, investing, and financing activities. This amount is added to the beginning cash balance to arrive at the ending cash balance.

The indirect method is widely used by companies as it relies on the net income figure, which is readily available from the income statement. It also provides insights into the adjustments necessary to convert net income to cash flows, highlighting the impact of non-cash items and changes in working capital on the company’s cash position.

How Odoo ERP composes the Cash Flow Statement?

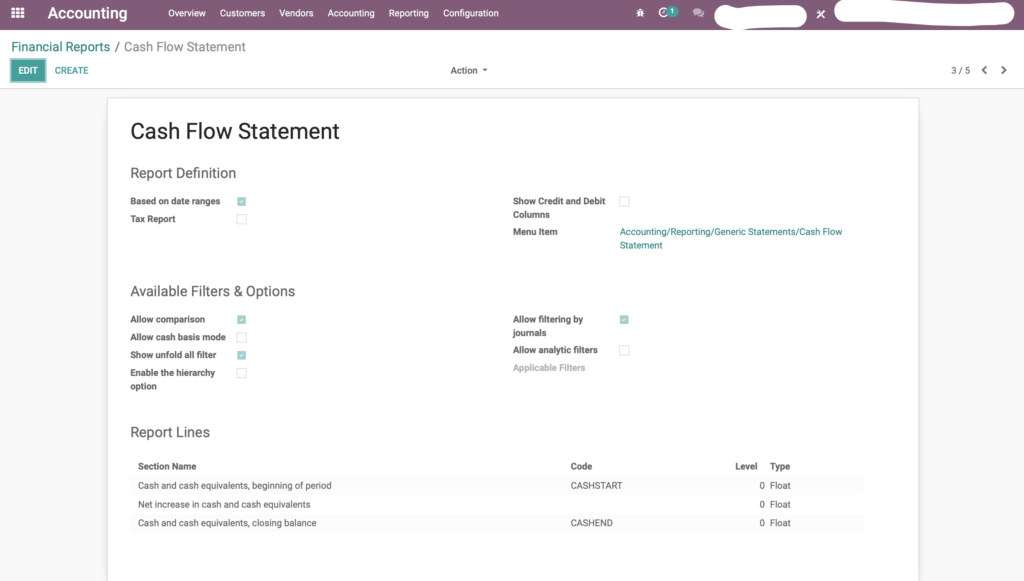

Odoo ERP, a comprehensive enterprise resource planning system, provides functionality for managing financials, including the generation of financial statements such as the Cash Flow Statement. While the exact process may vary depending on the specific configuration and customization of Odoo, here is the list of factors may impact Cash Flow Generation with Odoo:

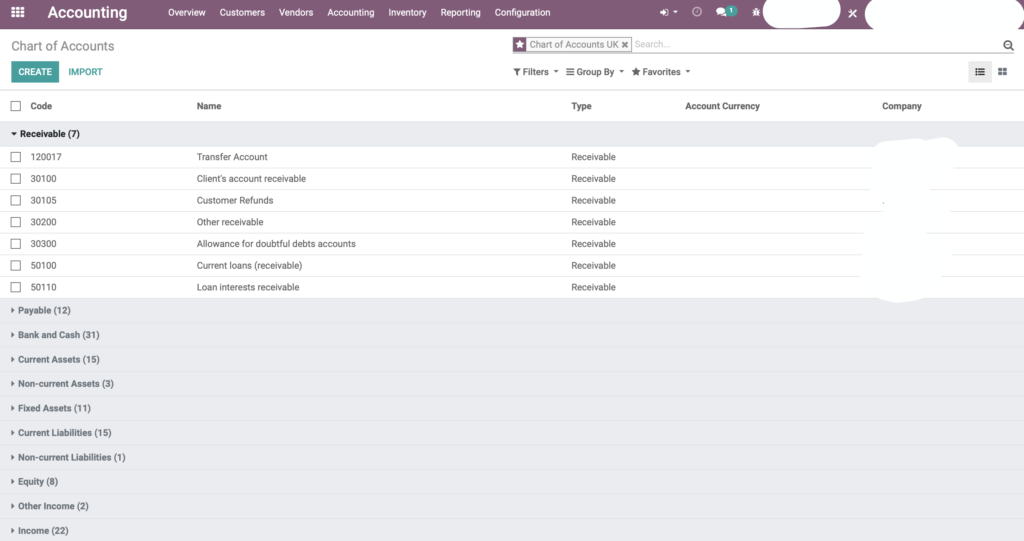

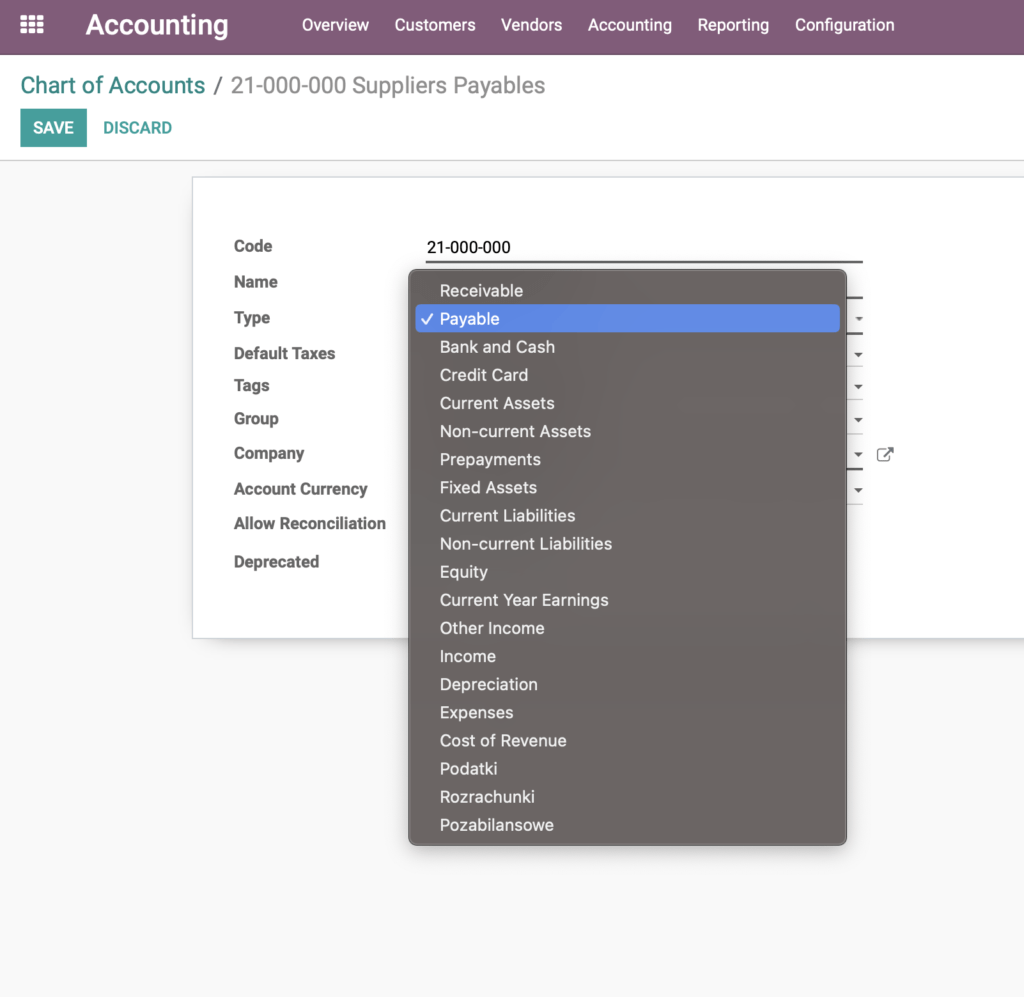

- Chart of Accounts and Account Types

Odoo allows you to set up and configure a Chart of accounts, which is a structured list of all the accounts used to record financial transactions in the system. The Chart of accounts includes various Account Types as Current Assets, Current Liabilities, Receivable, Payable, Bank and Cash, Equity, Income, Expenses, etc. It serves as the foundation for generating financial statements, including the Cash Flow Statement. - Account Tags

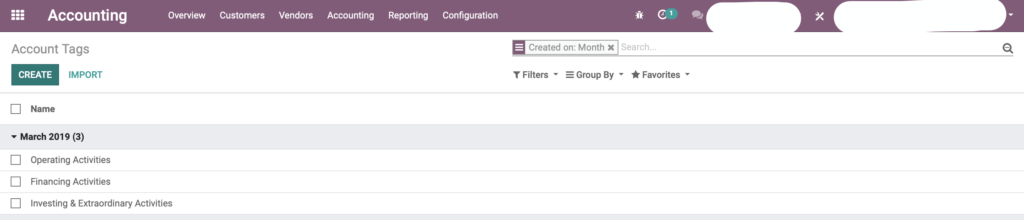

By default Oddo provides you with the simple list of Account tags that corresponds with the sections of Cash Flow Statement:

– Operating Activities

– Financial Activities

– Investing & Extraordinary Activities

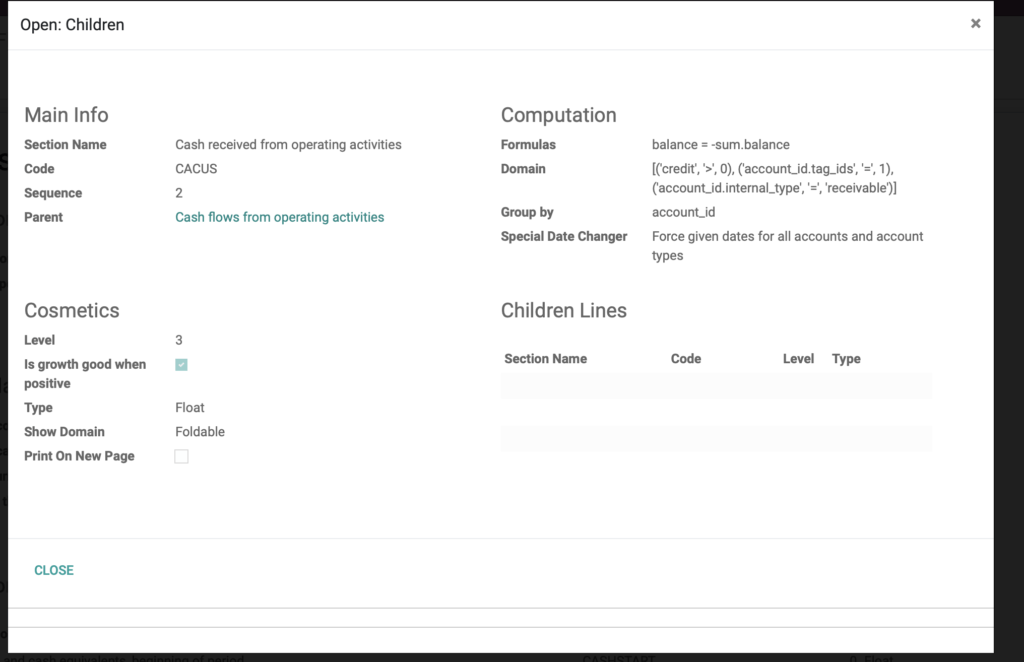

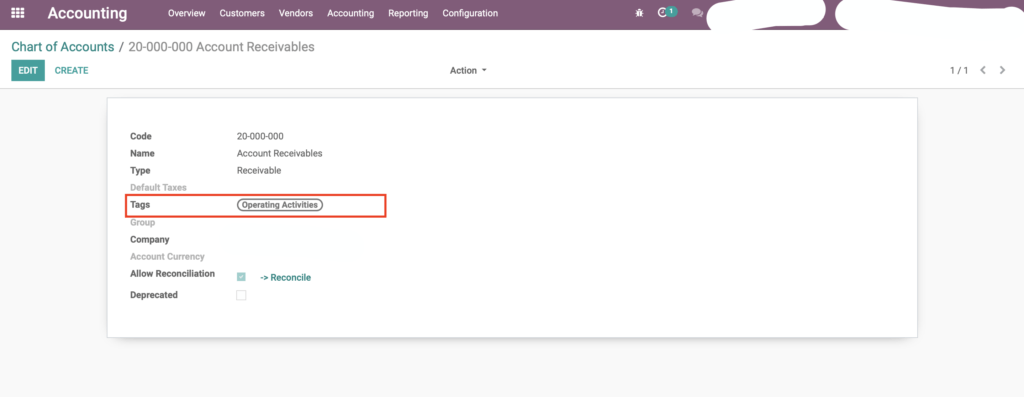

Odoo uses these tags in order to split your operations and transactions between Cash Flow Statement sections. A user must assign an Account Tag to Account in order to use Cash Flow. - Cash Flow Statement formulas and settings.

Odoo 12 is the latest version where a user had the option to Edit/Change Cash flow statement settings. From Odoo 14 and later there’re no any options to change these settings. Odoo Team confirmed that Cash Flow statement is hard coded also. We don’t have any ideas why Odoo team did such things. In order to change Cash Flow settings a customer has to request Odoo customisation services.

Account Types in Odoo ERP are hard coded and a developer only may change this list.

erpixel.com Team

Account Tags are not card coded, a user may change it. But Odoo account_tag_id in order to compose Cash Flow. Do not delete Account Tags! If you need to edit the list of Account Tags then activate Developer mode.

The lis of accounts in Odoo Chart of Accounts:

List of Account Tags created by Odoo:

Account Tag is assigned to an account:

We’re Official Odoo partner and provide Odoo Development services globally.